Through the 10th Amendment of the Income Tax Rules 2059, made on 2076 B.S. Nepal government has added a clause to add a contribution to Social Security Fund as a deductible expense. Notice was published in the Gazette on 2076/11/12.

According to the new amendment, a person contributing to the Social Security Fund established per Social Security Fund Act, 2074 can deduct a minimum of

a) contributed amount maximum up to NRs. 500,000 or

b) 1/3rd of Assessable Income

What does it mean?

It means a person who hasn't yet started a contribution to Social Security Fund or limited contribution to approved retirement funds such as Provident Fund and Citizen Investment Trust are availed existing deduction which is minimum of

a) contribution amount up to NRs. 300,000 or

b) 1/3rd of Assessable Income

And, those contributing to Social Security will get an additional deduction of NRs. 200,000 (from NRs. 300,000 to NRs. 500,000) provided 1/3rd of his/her assessable income is higher than NRs. 500,000.

Does this mean person contributing to Citizen Investment Trust and Social Security Fund will be availed NRs. 500,000 combining contribution to both CIT and SSF? The answer is no, a person can choose between one of the two. Either CIT hence, NRs. 300,000 or SSF and NRs. 500,000.

Does this mean person contributing to Citizen Investment Trust and Social Security Fund will be availed NRs. 500,000 combining contribution to both CIT and SSF? The answer is no, a person can choose between one of the two. Either CIT hence, NRs. 300,000 or SSF and NRs. 500,000.

Here's how Rule 21 should be read now:

अवकाश योगदानको सीमा: कुनै आय वर्षमा स्वीकृत अवकाश कोषको हिताधिकारी प्राकृतिक व्यक्तिले अवकाश कोषमा अवकाश योगदान गर्दा तीन लाख रुँपैया वा निजको निर्धारणयोग्य आयको एक तिहाईमा जुन घटी हुन्छ सो रकमसम्म आफ्नो कर योग्य आयबाट घटाउन सक्नेछ ।

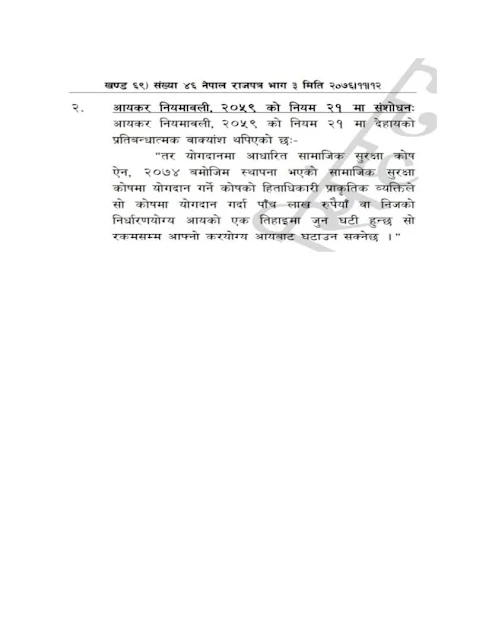

तर योगदानमा आधारित सामाजिक सुरक्षा कोष ऐन, २०७४ बमोजिम स्थापना भएको सामाजिक सुरक्षा कोषमा योगदान गर्ने हिताधिकारी प्राकृतिक व्यक्तिले सो कोषमा योगदान गर्दा पाँच लाख रुँपैया वा निजको निर्धारणयोग्य आयको एक तिहाईमा जुन घटी हुन्छ सो रकमसम्म आफ्नो कर योग्य आयबाट घटाउन सक्नेछ ।

Here's the notice published in Gazette for your reference.